Who would have thought that the stock market would be up this year? Not me. Not with everything that’s happened. Trump unveiled his tariffs at the start of April 2025. Everyone knew they were coming, but the world reacted surprised, including the stock market. More on the market decline later in the article. Let’s start with a recap.

For the past two years I’ve been using my HELOC to invest in two different ETFs.

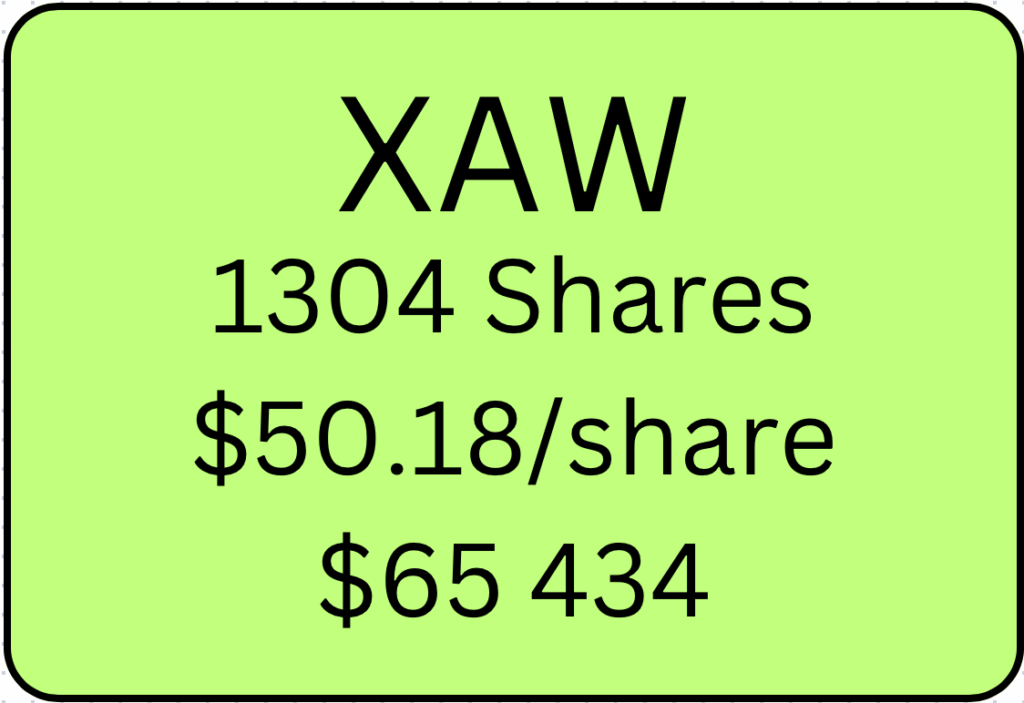

XAW (85%) – iShares Core MSCI All Country World ex Canada Index ETF

VCN (15%) – Vanguard FTSE Canada All Cap Index ETF

If you’re curious to see where this HELOC investing experiment began, please check out these previous posts.

HELOC Investing Update 2024 – A Year in Review

HELOC Investing Update – March 2024

How to Invest Your House in the Stock Market

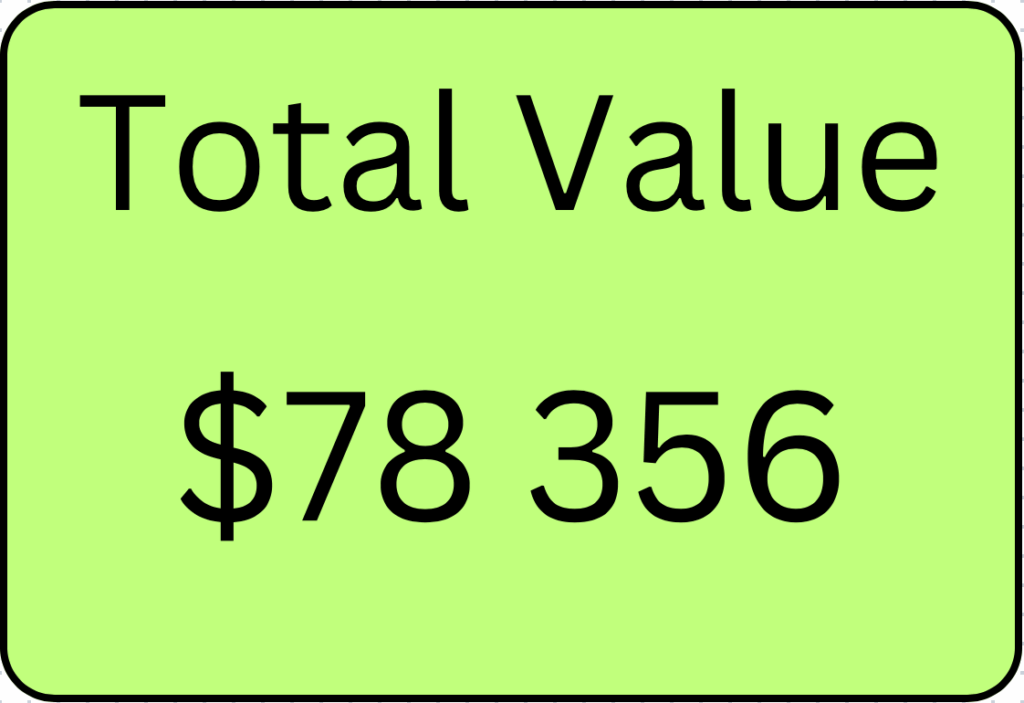

Below is the current value of my XAW and VCN holdings.

Total stock market returns have been fantastic. It is unlikely to continue like this. Stocks always revert back to the mean so I’m bracing for some bad or underperforming years ahead. This isn’t a short term wealth building strategy.

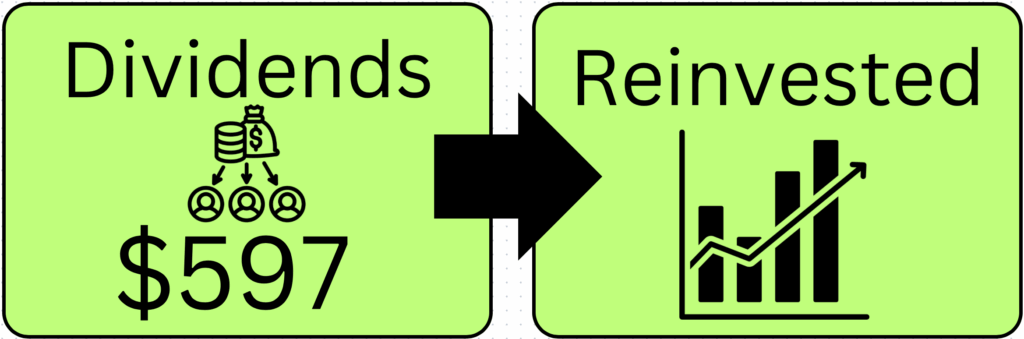

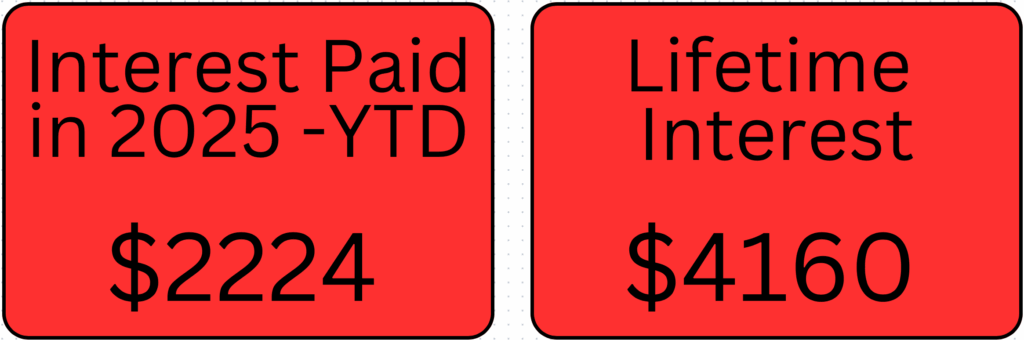

But even in underperforming years, stocks pay dividends. In this HELOC investing portfolio, XAW pays dividends twice a year and VCN pays quarterly. I’m waiting for one more dividend payout at the end of December from both funds. That will push annual dividend payments close to $1000.

With leveraged investing, there are opposing forces acting on your portfolio. The good ones are capital growth and dividends. These are what we want. But when money is borrowed to invest, interest payments are needed to service the debt. In addition, the borrowed money will eventually need to be paid off.

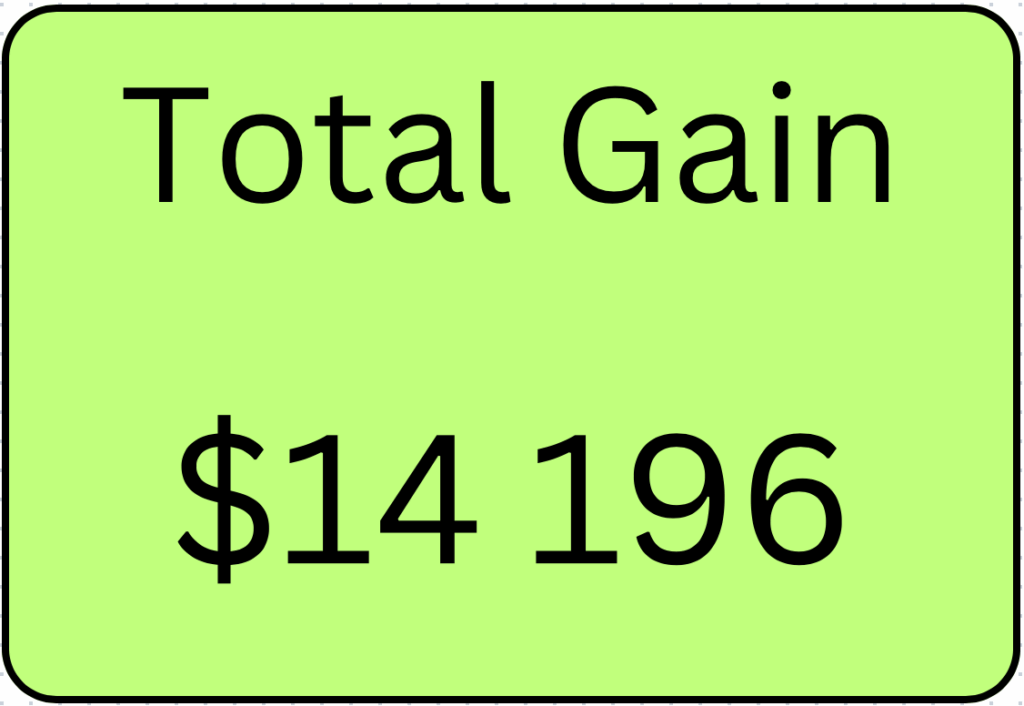

Here’s how you calculate the total gain.

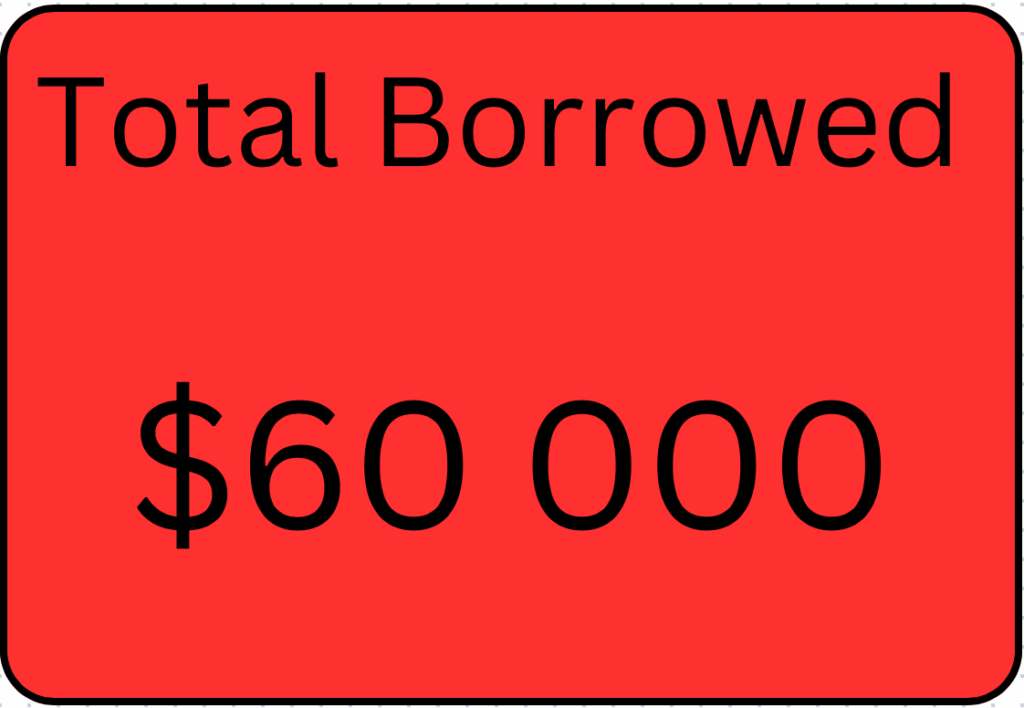

$78 356(Investment Account) – $60 000(HELOC balance) – $4160 (Total Interest) = $14 196

All in all, my portfolio is up a total of roughly $14 000. Two things I didn’t include in this calculation were my potential tax refund from the interest payments, and the tax that I’ll need to pay on the dividends. The tax refund will be more than the tax owed on the dividends.

I pay approximately $300/month to service the loan. These are interest only payments so the loan balance stays at $60 000. But I just learned something new that could be helpful in the future.

When I started investing with my HELOC I thought I couldn’t capitalize the interest. My understanding was that you needed a readvanceable mortgage to do that. I was wrong.

You can withdraw the exact amount of the interest payment to your chequing account. Then turn it around and pay the interest on the HELOC. This is good to know because there could be a time that I can’t make the $300/month payment.

The benefits of capitalizing the interest is that it doesn’t affect your cash flow. The kicker is that I need enough room in my HELOC to pay the interest if I choose to go that route. Right now I’m comfortable paying the monthly interest payment of $300.

I want to write about the major investing event that happened this year and how it affected my HELOC investment account.

April Tariff Fiasco

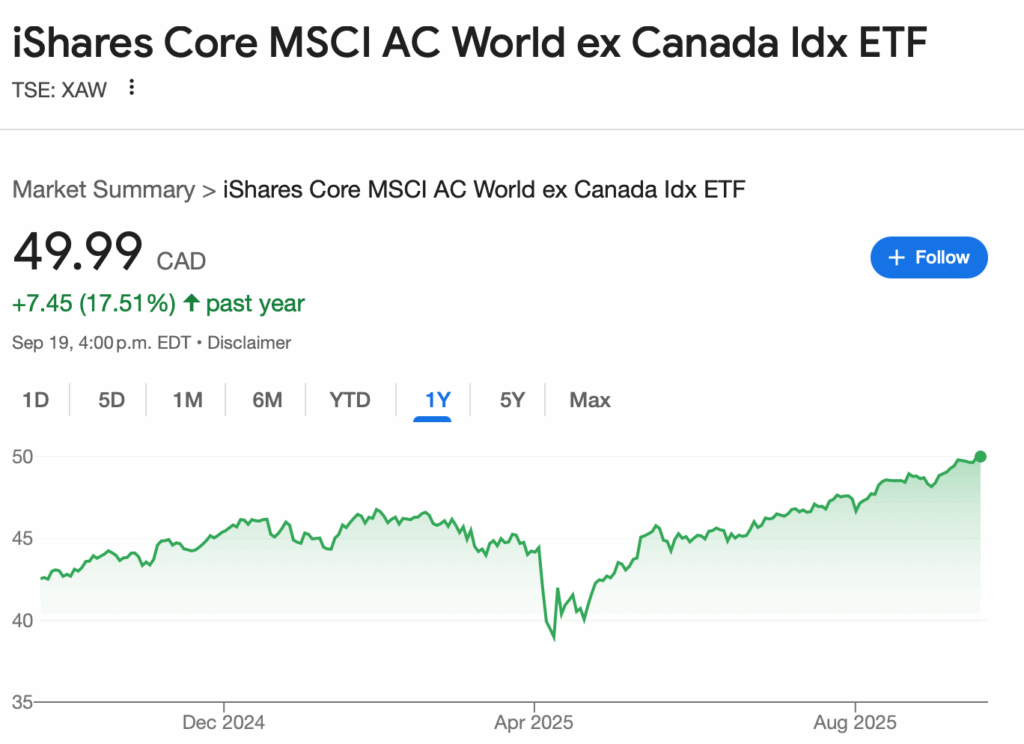

When Trump announced his Tariffs were going in to effect, I didn’t think it was a big deal. That is until the stock market started to drop for multiple days in a row. I’m not going to lie, it’s scary when this happens. There’s always a thought in your head that wants to sell. It’s painful to ‘lose’ money so quickly.

At the bottom in April, all my HELOC investing gains were wiped out. It hurt! But I knew the right thing to do. The market always recovers and when it’s down, it’s best to lean in and invest more when prices are at a discount.

Notice how I said market. I didn’t say stocks. Gains from stocks do get wiped out. They get wiped out all the time and never return to their previous highs. I don’t like those risks. That’s why I invest in market index funds that span the entire world.

Sitting here looking at these charts in hindsight the sudden drop doesn’t look like a big deal. But when you are living through it and watching your portfolio lose money every day, it’s all you can think about.

I knew this moment was going to happen eventually. All my investing gains were wiped out when the market bottomed on April 8.

I felt sick to my stomach. Losses suck! Even though I knew moments like that were coming, it’s still difficult to stay focused on the goal. As the saying goes, but this time it’s different.

This was my chance to deploy more of my HELOC.

On April 4th I invested $5000 into XAW (85%) and VCN (15%).

On April 7th I invested $5000 in XAW (85%) and VCN (15%).

On April 8th I invested $5000 in XAW (85%) and VCN (15%).

I decided to stop there because I thought the market might continue to drop. However, it hit the bottom on April 8th and then started its march to new highs. You never know where the bottom is going to be. It’s impossible to predict.

In hindsight, I should have invested more but it’s scary when the market drops so quickly. Since April 2025, I haven’t invested anymore funds using my HELOC.

Conclusion and Takeaways

All in all it’s been a good year for HELOC investing. I’m approaching 2 full years of borrowing to invest which coincidentally coincided with two great years for the stock market.

I know that this run can’t keep going and stocks will eventually revert back to their mean returns. 20% gains are addictive but unrealistic long term.

I’m doing this for the long term so I expect many more bumps in the road.

The most important thing to do is NOT SELL!!! I’m telling this to myself so the next time it happens I don’t panic.

Challenges moving forward are to keep paying the monthly interest payments on the $60 000 loan.

To wrap up, none of this is investment advice. I’m documenting this strategy to keep me on track and to minimize mistakes. Please do your own research and gather information from multiple sources. Until next time, Happy Investing!